Q2 Thrive Newsletter

It was Ralph Waldo Emerson who said, “The first wealth is health” and it could not be truer today. The advancements in medicine and the technologies associated with it have increase the average lifespan over 6 years in just a 30-year period...an increase of almost 10%! This is great news but not something to be complacent about. The reality is the life expectancy figures are based on average and in many cases how you take care of yourself over your lifetime will have a direct impact on your longevity. For example, a male age 65 that takes care of them self has a one and three chance to live to age 90 and a female has almost a one in two chance!

It was Ralph Waldo Emerson who said, “The first wealth is health” and it could not be truer today. The advancements in medicine and the technologies associated with it have increase the average lifespan over 6 years in just a 30-year period...an increase of almost 10%! This is great news but not something to be complacent about. The reality is the life expectancy figures are based on average and in many cases how you take care of yourself over your lifetime will have a direct impact on your longevity. For example, a male age 65 that takes care of them self has a one and three chance to live to age 90 and a female has almost a one in two chance!

Regardless of how much wealth you have built or are building without your health there is no way to enjoy it. Be vigilant and proactive instead of delay and be reactive. Here are some basic tips to keep you on the right track.

- Get an annual physical...I know it's not fun but important.

- Talk to you doctor about vitamins, minerals and other natural supplements will help your situation

- Get your eyes checked at least annually

- Exercise with purpose based on your doctor's guidance...don't forget to work on balance and core strength

- Don't forget to exercise your brain-mental stimulation and life learning new things help maintain mental sharpness.

As with anything health related always consult your doctor(s) before making any major change;and don't forget to make staying healthy fun whether it be trying new recipes or exploring new ways to get excercise. There are infinite paths to optimal health, the tough part is finding the one that works best for you.

Inflation is on the mind of many Americans. Boomers and some Gen Xers have seen high inflation before, but younger Americans are facing an entirely unfamiliar economic landscape.

While past performance is certainly not indicative of future results, there's a lot we can all learn from the last substantial inflationary period in the U.S., which began in the mid-1970s and peaked in 1980.

U.S. consumer inflation data is measured most frequently by the Consumer Price Index (CPI). According to the U.S. Bureau of Labor Statistics (BLS), CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

In April of 1980, the annualized CPI rate peaked at 14.76%. At the same time, unemployment had jumped to 6.9% amid a recession. The Federal Funds rate (the rate set by the Federal Reserve for overnight lending) ranged between 14.3% and 19.85% in April 1980.

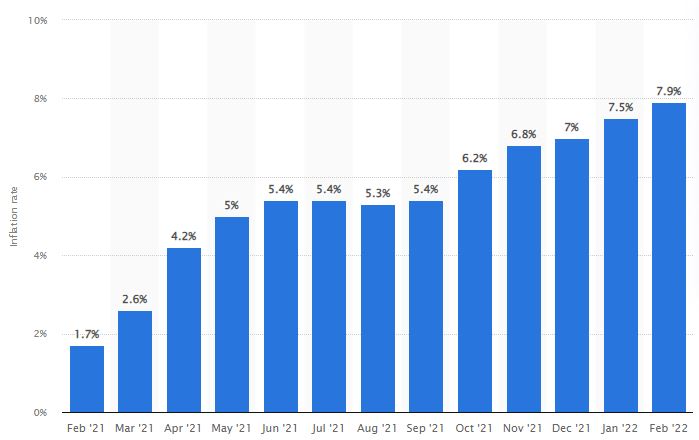

In comparison recent 2022 CPI data released in March showed that consumer inflation increased by 7.9% in February 2022. So, according to this data, what cost $100 a year ago now costs $107.90 (on average across all categories). The consumer inflation data is further broken down by sectors such as food and energy. Recent unemployment data shows a 3.8% unemployment rate.

You might be thinking that doesn't seem so bad compared to 1980. But it's important to note that inflation just started being an issue in April 2021. (See chart below) The last time the U.S. faced high inflation, there was a slow lead-up. For comparison's sake, the United States had very low inflation levels between 1962 and 1973, before inflation reached current levels–around 7.9%–beginning in 1974. After that, inflation continued to climb, and the U.S. experienced high inflation levels until 1981 and late 1982. The question then becomes: Are we set to see a similar upwards climb? The answer remains murky.

The Takeaway

Inflation will more than likely continue to persist throughout 2022 with added pressure due to the conflict in Europe. In addition, many economists believe higher inflation is here to stay for a period of time but hopefully not at the levels we are currently experiencing. From our standpoint, we have and will continue to make any needed portfolio adjustments to reduce the effects of inflation on your retirement assets.

New Required Minimum Distribution Tables

The IRS has released new life expectancy tables for calculating required minimum distributions (RMDs) for 2022. The most commonly used tables are the Uniform Lifetime and the Single Life Expectancy Tables. The Uniform Lifetime Table is used by most IRA owners who need to take 2022 lifetime RMDs. The Single Life Expectancy Table is used by IRA beneficiaries who must take an annual RMD for 2022. Click here to see a copy of the new minimum distribution tables.

The new tables reflect longer life expectancy factors. For example, a 72-year-old with $100,000 IRA balance would have a minimum distribution of $3,906 in 2021. In 2022 a 72-year-old with a $100,000 balance would have a minimum distribution of $3,650.

Takeaways

With the new table less taxable income is forced out of retirement accounts thus reducing taxable income slightly. In contrast, a reduction in minimum distributions means more value stays in your IRA and grows and is fully taxable at your tax rate not capital gains rates. With that said there is no action needed by you as we calculate your RMD amount and make sure it's distributed prior to the year end.

I wanted to touch base about the conflict in Russia-Ukraine—specifically, the cyber-attacks that recently hit the country of Ukraine both leading up to the Russian invasion and after the conflict began.

The first major DDoS attack on February 23, 2022, took down several government and banking websites. If you're not familiar, a DDoS attack happens when a hacker overwhelms a victim's network or server with traffic so that others are unable to access it. Another wave of attacks followed on February 28, once again shutting down multiple Ukrainian government websites.

As the conflict continues, cybersecurity experts are bracing global leaders for more attacks of this kind. On March 21st President Biden urged private companies to “Harden your cyber defense immediately.”

The bottom line is you can make basic adjustments to help protect yourself. Below are a couple basis ways to improve your cybersecurity.

Strengthen passwords

Nonsense passwords with strings of letters, numbers, and characters aren't as secure as you think they are. Here's why:

- First, they're hard to remember.

- Second, when forced to reset a password, people are hesitant to throw away the time they spent memorizing the one they have. In light of that, they only make a slight change to their current password making it easy for hackers to take advantage.

A stronger option for individuals and businesses of any size is the use of “passphrases” over nonsense passwords. Passphrases meet complexity requirements and are easier to remember, too. Just consider the difference between “IgbH$90l@!” and “Blue cats, meow loudly!”

Your action item? The next time you're prompted to create or reset a password, go with a passphrase. Chances are you'll remember it more easily and keep hackers frustrated — exactly where you want them to be.

Use Anti-Virus Software (and keep it up to date)

There are numerous types of ant-virus software that contains other protection against phishing and malware but beware as some are considerably better than others. Click here to view a review by PC Magazine of personal computer anti-virus software.